Introduction

In this age of international mobility, cross-border successions (i.e. the devolution of one’s estate involving one or more foreign elements) are common. These situations prove particularly complex and stressful when they have not been properly anticipated (at the planning stage), or when they are not handled methodically (at the settlement stage).

In the event of a death occurring abroad or where assets are located in several countries, who are the persons entitled to inherit? What are their rights? What taxes will they have to pay and where? How can this situation be resolved quickly, whilst minimising the risk of family conflict? These questions, far from being theoretical, affect many families on a daily basis.

This is why this article aims to raise our readers’ awareness of French cross-border succession law. Whether you are a beneficiary of such an estate (e.g. because your parents live abroad), or you are wondering about the fate of your estate after your death (e.g. when moving abroad), certain basic precautions must be taken.

The practical guide that follows will deal successively with the civil aspects (i.e. the rules determining the distribution of assets to heirs and legatees) and the tax regime (the duties that the latter must pay to the authorities) of cross-border inheritances connected to France. However, we will not address the contentious settlement of such estates, i.e. where a dispute between several heirs, beneficiaries and/or legatees must be resolved through the courts.

I – The civil aspect of cross-border successions

1.0. Some definitions

To fully appreciate the Civil aspects of cross-border successions, technical concepts and terms must be understood. You will find below the glossary we use on a daily basis to handle our cases. In this article, the following concepts or terms (indicated by capital letter) will have the meanings specified in the table below:

| Concept or term | Definition (Citizen Avocats) | Comment |

| Acte de notoriété | Refers to the official document, drawn up by a French notary, which establishes a person’s status as an heir, legatee or beneficiary under the Law applicable to the succession (whether French or foreign). | Under French law, it is the central document that formalises the amicable settlement of a succession. |

| Civil aspects of a succession | Refers to all subjects related to the mortis causa devolution of assets, governed by the Law applicable to the succession (whether French or foreign), such as inter alia: – the validity of a will, – the inheritance rights and entitlements, – the reserve héréditaire (if any), – the mandatory modalities and formalities for settling the estate, etc. | In this regard, determining the Law applicable to the succession is of fundamental importance. In any international succession, the applicable law must be determined as a matter of primary importance. |

| Conflict of jurisdiction | Refers to the problematic situation in which an international succession dispute raises the question of the concurrent jurisdiction of the courts of several States, due to the links that the dispute has with them. | In practice, this question arises when the claimant brings legal proceedings (‘which court should I bring this dispute before?’) or when the defendant challenges the jurisdiction of a court or the validity of a decision (‘this court does not (did not) have jurisdiction to hear this dispute’). In any international succession dispute, the conflict of jurisdiction must be resolved as a matter of absolute priority, in order to bring the case before the correct court. |

| Conflict of laws | Refers to the problematic situation where the law applicable to an international succession is unknown, as that succession is connected to the legal systems of several states. | For any international succession, the Law applicable to a succession must be determined as a matter of absolute priority, both upstream (i.e. at the planning stage) and downstream (i.e. at the settlement stage). |

| Law applicable to the succession | Refers to the national law (in principle, a single law) governing all the Civil aspects of a succession, as designated (since 2015) by the Rome IV Regulation. | As per the Rome IV Regulation, the Law applicable to a succession governs its Civil aspects, but has no bearing on the Tax regime of the succession. |

| Rome IV Regulation | Refers to Regulation (EU) No 650/2012 of the European Parliament and of the Council of July, 4th 2012 on jurisdiction, applicable law, recognition and enforcement of decisions and acceptance and enforcement of authentic instruments in matters of succession and on the creation of a European Certificate of Succession. | The Rome IV Regulation is one of the most effective instruments of private international law at European level. It resolves Conflicts of jurisdiction and Conflicts of law in matters of succession. This Regulation determines the Law applicable to a succession. It governs only Civil aspects and has no bearing on the Tax regime of the succession. |

| Habitual residence at the time of death | An autonomous concept of private international law which, in the absence of any choice of law (express or implied) made by the deceased, determines the Law applicable to the succession. | This concept is relevant only for determining the Law applicable to the succession. It cannot and must not be equated with concepts derived from French tax law or bilateral tax treaties (such as the ‘foyer’ for example). |

1.1. 1st good practice: putting together a qualified international team

There is no doubt, in our mind, that the human factor is the most significant determinant of the efficiency and compliance of the settlement of an international estate.

In practical terms, who will be the professionals – the men and women – handling the case? If the beneficiaries engage qualified professionals who are duly authorised to practice law in their respective countries and are genuinely international-minded, the Civil aspects will be settled efficiently and the Tax regime will be complied. If, on the other hand, they call upon unregulated or incompetent professionals, the succession is likely to become a real nightmare, dragging on indefinitely and incurring excessive costs.

The author of these lines is aware that he is ‘singing his own praises’ here. Nevertheless, it remains absolutely indisputable that the entire efficiency of the process depends on the competence and proactivity of the professionals involved.

The coordination of different national procedures (e.g. judicial probate in common law systems and the Certificat de notoriété drawn up by a notary in civil law systems) requires seamless coordination between the professionals involved. Whether it involves preparing certificates of custom and other legal opinions, affidavits or expert witness statements, the production of high-quality certified translations, or the recognition of powers conferred under foreign law upon certain individuals (for example, theEnglish executor, whose prerogatives must be formalised in France prior to certain acts), the key word is coherence.

Franco-French or purely British practices must be avoided at all costs. Seeking to resolve everything according to one’s own law, whilst disregarding foreign elements, is not only contrary to private international law (and therefore illegal), but also entirely inappropriate in a cross-border context. The practice of private international law, a fortiori when resolving legal situations arising upon a person’s death, requires an open mind, professional coordination, flexibility and transparency. One cannot force one’s way through a cross-border inheritance case!

1.2. 2nd good practice: determining the law applicable to the succession

The Rome IV Regulation enshrines the principle known as the ‘unicity’ of the Law applicable to the succession. This means that, where the conditions for the application of this Regulation are met, a single law applies to the entire succession, regardless of where the assets are located.

This law is, by default, that of the Habitual residence at the time of death (Article 21 of the Rome IV Regulation).

‘By default’, because the Regulation enshrines a fundamental freedom: that of choosing one’s national law to govern one’s future succession. Article 22 ‘Choice of law’ indeed provides that:

1. A person may choose as the law to govern his succession as a whole the law of the State whose nationality he possesses at the time of making the choice or at the time of death. A person possessing multiple nationalities may choose the law of any of the States whose nationality he possesses at the time of making the choice or at the time of death. 2. The choice shall be made expressly in a declaration in the form of a disposition of property upon death or shall be demonstrated by the terms of such a disposition. 3. The substantive validity of the act whereby the choice of law was made shall be governed by the chosen law. 4. Any modification or revocation of the choice of law shall meet the requirements as to form for the modification or revocation of a disposition of property upon death.

Whilst the Regulation does indeed allow the testator to make a professio juris, that is to say, to choose the Law applicable to his/her succession, this choice may only relate to a law of which he/she is a national.

1.3. 3rd good practice: checks regarding the French résérve héréditaire

The reserved portion of an estate is the share of the deceased’s estate that French law guarantees will pass to certain heirs, known as heirs héritiers réservataires. This share cannot be freely disposed of by will. Only the remaining portion of the estate, known as the quotité disponible, may be freely bequeathed to other persons.

We have already covered this topic in several articles.

We will therefore simply reiterate that, when the Law applicable to the succession is French law, or where the persons concerned by this succession are nationals of a Member State of the European Union or habitually resident there and

assets are situated in France, the implications of the reserved portion must be taken into account.

Let us take a simple example:

Dennis was an American citizen, originally from the state of Georgia, but married to a French woman. He died in 2025. His Habitual residence at the time of death was in France, as he had been living in the Dordogne for over ten years.

He is survived by two children from a previous marriage, who are both Tax residents of California. Due to a family dispute, Dennis lost contact with them during his last years. As they hold prestigious positions in Silicon Valley, Dennis considered them sufficiently wealthy. This is why his will (which explicitly refers to the laws of the State of Georgia) provides for 70% of his assets, wherever located, to be bequeathed to his wife and 30% to a French friend of his.

However, although the wills are subject to a law permitting disinheritance (the law of his US nationality, and more specifically that of his state of birth, Georgia), the children will in this case be entitled to claim a compensatory share amounting to up to 66.66% of the value of the total estate from the assets located in France. This catastrophic consequence for the beneficiaries should have been anticipated, as it now entails a very high risk of inheritance disputes….

1.4. 4th good practice: identifying ‘UFOs’

In one of our legal opinions, we described a dynastic trust under English law established in 1925 as an ‘unidentified flying legal object’ in the sense that it did not fit into any ‘box’ of French civil or tax law applicable ratione temporis. The situation was problematic, as our client, the beneficiary of part of the trust’s corpus,which the trustees were responsible for distributing, had established their Tax residence in France. We therefore had to address a two-fold question: how should this transaction be classified legally? What taxes, if any, are payable in France?

A technical legal opinion, followed by several tax rulings, was required in order to identify the legal framework applicable to this dynastic trust.

In another case, where we were tasked with assisting a Franco-American widow, we realised that the deceased’s estate was now held in a trust governed by the law of New Mexico.

The first problem was that French assets, notably real estate (normally governed by the lex rei sitae with regard to the transfer of ownership), had been transferred into the American legal trust wrapper.

The second issue was this atypical trust was ‘non-triangular’: both grantors were also trustees and beneficiaries of the trust. This triple designation served a pragmatic purpose: to allow each spouse to manage, administer and dispose of all the joint assets with complete freedom during their lifetime. The triangular relationship characteristic of Anglo-Saxon trusts was therefore largely theoretical, since, in the interim until the second death, the trust assets were not entrusted to a third party for the benefit of any other.

How could this unusual succession be settled?

The first step was to assemble a high-level international team. We contacted a bilingual French notary specializing in private international law, as well as a US attorney qualified in trusts and probatefrom New Mexico. The latter quickly produced a legal opinioncertifying that the trust had been validly established under the Law applicable to the succession. Reasoning by analogy and drawing parallels with the civil law concepts applicable in France, we then concluded that this trust, in practical terms, had the same effect as a a French legs universel entre époux. On the basis of these two legal opinions, the notary then drafted a technical Certificat de notoriété, before proceeding with the relevant tax declarations acknowledging a full exemption from inheritance tax in favour of the widow, as we had concluded. Within a few weeks, a particularly complex Franco-American succession was settled, without the slightest civil or tax obstacle.

There are numerous examples of international situations where a mechanism unknown to French law (in this case, the trust) must nonetheless produce effects (in this case, a gratuitous transfer) within our territory, without overlooking their cross-border tax consequences.

In the presence of such ‘UFOs‘, caution is advised. Various tools are available or may even be ‘invented’ for the occasion.

In the face of these complexities, there is an “urgency not to rush anything”. A detailed legal consultation enables one to untangle the knot, that is to say, to clearly define the issues, apply the law to the specific case, identify effective solutions, and then implement a coordinated strategy. It’s obviously better to dedicate a month or two to the rational coordination and settlement of a cross-border estate rather than charging ahead blindly and making irreparable mistakes that it will take years to repair…

The additional complexity of the ‘UFOs‘ must therefore be taken into account from the very outset of the case. Ignoring it, downplaying it, or attempting to force the issue will only increase the risk of inheritance disputes, or cause a tax reassessment. In the presence of such foreign legal entities, caution and rigour are essential.

For further information on the legal treatment of foreign trusts in France, please refer to our guide:

II – The tax treatment of cross-border successions

2.0. Some definitions

To fully understand the tax implications of cross-boder successions, certain key concepts and terms must be understood. Below, you will find the glossary we use on a daily basis in this field. The following concepts or terms (indicated by a capital letter) will have the meanings specified in the table below:

| Concept or term | Definition (Citizen Avocats) | Comment |

| Tax regime of an estate | Refers to the set of national and international rules used to determine the duties that tax authorities may levy on the estate. | Determining Tax jurisdiction is fundamental in this regard. Although connected to the Civil aspects of an estate, the Tax regime is independent of these in that it pursues different objectives and is governed by its own rules, principles and definitions. |

| Tax jurisdiction (of a national administration) | Refers to the legitimate authority of a national tax authority (eg, the DGFIP or HMRC) to tax assets, revenues, or an estate under its own national laws and/or as per the provisions of a bilateral agreement. | Bilateral agreements serve, in particular, to avoid double taxation by granting General tax jurisdiction to one country rather than the other. |

| General tax jurisdiction | In the context of a cross-border inheritance, this concept refers to the general power to tax, by default, the entire estate, subject to specific exceptions (generally due to the geographical Location of assets) relating to the deceased’s estate and/or the transfer made to the heirs, legatees or beneficiaries. | In the bilateral conventions applicable to inheritance tax signed by France, the Last domicile is generally the determining criterion enabling a tax administration to establish its General tax jurisdiction. |

| Tax residence or tax domicile (of a living taxpayer) | Refers, in the context of France, to the fact that a person is liable for French tax on their global income and subject to a general obligation to file a tax return due to their personal circumstances having objective links with that country, such as: their Foyer or Main place of residence, the pursuit of a professional activity, the centre of their economic interests, or the specific situation of civil servants… | In French tax law, the concept of Tax residenceis defined in Articles 4 A and 4 B of the Code general des impôts. Article 4 A establishes the general principle that: a person whose tax domicile is in France is liable for tax on all their income, whether from French or foreign sources (unlimited tax liability), whereas a person whose tax domicile is outside France is taxable in France only on their income from French sources (limited tax liability). However, this article is subject to any contrary provision in a bilateral agreement in force. |

| Last domicile (of the deceased) | Refers to the country where the deceased is considered to have been domiciled at the time of his/her death, based on objective criteria that depend solely on factual circumstances and legal and/or conventional rules, and in no case on the deceased’s personal wishes and decisions, the Law applicable to the succession, his/her previous declarations, or even, in absolute terms, the Tax residence determined during his/her lifetime. The Last domicile is a fundamental concept in international tax law because, once established, it determines the General tax jurisdiction and, by extension, the Location of certain assets. | This concept is primarily relevant for determining General tax jurisdiction under bilateral treaties specifically applicable to the elimination of double taxation in relation to inheritance tax. The bilateral conventions signed by France generally refer to national definitions (which implies, de facto, an assimilation to Tax residence). If the deceased can be considered domiciled in both countries under their respective laws, the concept of Last domicile becomes an independent one. In practice, the last Tax residence and the Last domicile are almost always identical. Nevertheless, these concepts are technically distinct, as they correspond to different definitions and uses. The distinction between these concepts is mostly relevant when uncertainty arises post mortem regarding the deceased’s Tax residence. This is especially the case when it appears that the deceased had committed fraud in this regard during their lifetime… |

| Foyer | Under French law, the place where the taxpayer or their family normally lives (the family’s usual place of residence: spouse and children). | This is one of the objective criteria set out in Article 4 B of the Code general des impôts for establishing Tax residence in France. It is independent of the Main place of residence if the family resides in France. |

| Principal place of residence | A criterion based on the taxpayer’s actual physical presence on French territory for more than 183 days in the course of a year. | This criterion is used by the French tax authorities to determine Tax residence. It should not be confused with the Habitual residence at the time of death, which is used for Civil matters. |

| Location of an asset | In the context of cross-border successions, this term refers to the country where an asset is deemed to be situated under the bilateral convention, either through the application of specific criteria applicable to certain types of assets (for example, geographical location for immovable property), or by intellectual attachment to the Last domicile. | This criterion is fundamental, because only the assets Located in the territory of the State where the deceased did not have his Last domicile can be taxed there. |

| Tax credit | Refers to the mechanism for avoiding double taxation in the State with General tax jurisdiction, by deducting the inheritance tax levied in the other State on assets Located there. | Double taxation avoidance is first achieved through delimitation (Last domicile and Location of an asset), and then, secondarily, by applying a Tax credit to assets that remain subject to double taxation. |

2.1. 5th good practice: assessment of the territorial scope of French inheritance tax

Although this may seem somewhat paradoxical from a methodological perspective (since national tax laws are supplementary to bilateral conventions), the first question to ask regarding taxation, in a French cross-border context, is that of the French authorities’ Tax jurisdiction.

Article 750 ter of the Code general des impôts is undoubtedly the most important provision, as it sets out the criteria establishing the French authorities’ Tax jurisdiction by default (that is, in the absence of contrary bilateral clauses), namely the last Tax residence of the deceased, that of the heir, or the location of the assets.

To summarise:

- If the deceased was a French Tax resident: taxation of all assets transferred in France.

In this scenario, all assets transferred are taxable by default, whether they are located in France or outside France and whether the heirs, donees or legatees are resident for tax purposes in France or not (Article 750 ter, 1°).

In this case, the amount of transfer duties paid outside France will generally be deductible from the tax due in France.

- If the deceased was not a French Tax resident:

- If the heir or legatee is also not resident in France, only assets located in France are subject to French inheritance tax (CGI, Article 750 ter, 2°).

In this case, it won’t be possible to offset tax paid abroad against the tax due in France.

- If the heir or legatee has been resident in France for at least 6 years during the 10 years preceding the transfer, all transferred assets located in France or abroad are subject to French inheritance tax (CGI, Article 750 ter, 3°).

This six-year period within the 10 years preceding the chargeable event need not be continuous.

In this case, the amount of inheritance tax paid outside France will, in principle, be deductible from the tax due in France.

Let us take another practical example:

A widow dies, leaving as her sole heir her adult son, who is a French Tax resident. The total estate consists of €300,000 in French company shares and a villa in Greece valued at €400,000.

This gives a gross taxable estate of €700,000 – €100,000 (child allowance) = €600,000.

The French tax amounts to €122,000, but the villa is also taxed in Greece at a rate of 5%, amounting to €20,000.

In France, the €20,000 in Greek tax can be offset against the €122,000, resulting in a final tax liability in France of €102,000.

2.2. 6th good practice: identification and application of special bilateral agreements

The tax treatment of cross-border inheritances depends on whether or not there is a bilateral agreement aimed at eliminating double taxation in relation to inheritance tax and, where applicable, on the provisions of that agreement.

In practice, such specific bilateral agreements are unfortunately quite rare. Some countries with which France maintains strong economic, cultural and diplomatic ties still lack a treaty in force. We are thinking – much to our regret – of Mauritius or Switzerland, for example.

To avoid double taxation and clarify the allocation of taxing rights between states, France has concluded 36 special treaties covering inheritance tax. The countries concerned are as follows: Algeria, Austria, Bahrain, Belgium, Burkina Faso, Cameroon, Canada, Central African Republic, Congo, Côte d’Ivoire, the United Arab Emirates, Spain, the United States of America, Finland, Gabon, Guinea, Italy, Kuwait, Lebanon, Mali, Morocco, Mauritania, Monaco, Niger, New Caledonia, Oman, Qatar, the United Kingdom, Saint Pierre and Miquelon, Senegal, Sweden, Togo and Tunisia.

The material scope of these conventions may vary, as may the specific rules on apportionment they provide for. For example, whilst the special Franco-American convention applies to gifts, such is not the case with the Franco-British convention… It is therefore advisable to read each convention carefully, as they all reflect different bilateral relationships.

In practical terms, certain provisions grant exclusive taxing rights to the State with General taxing jurisdiction, whilst others reserve subsidiary jurisdiction for the State in which some assets are Located. This is what justifies the provisions on the elimination of double taxation through Tax credits.

2.3. 7th good practice: meeting declaration deadlines and tax compliance

The final point worth highlighting is compliance with the reporting and tax obligations inherent in any transfer of assets. Whilst, at the estate planning stage, seeking to optimise taxation is perfectly legitimate, it has no place at the stage of settlement. Put simply, after death it is too late to optimize. It is now time to scrupulously adhere to the applicable deadlines and fulfil reporting obligations, in the interests of compliance.

Typically, the deceased’s Last domicile must be precisely identified, based on objective factual circumstances. The temptation to retroactively ‘shift’ the deceased’s Last domicile in order to shift General tax jurisdiction to the most favourable country must be avoided, as it is fraudulent (!) Such an approach, however tempting, would expose the estate to a tax reassessment and heavy penalties! Let us repeat this again and again: when it comes to cross-border inheritance, the aim is compliance, not optimisation!

In France, this compliance is primarily demonstrated by filing an inheritance tax return with the relevant authorities (Article 800 of the Code general des impôts). The inheritance tax return remains mandatory and must be filed by the heirs even if no tax is due.

This declaration must be filed within six months of the date of death, where the death occurred in mainland France, or within one year for deaths occurring abroad (Article 641 of the Code général des impôts).

In the event of failure to file a return or late filing, several penalties may apply:

- Late payment interest at a rate of 0.20% per month, calculated from the first day of the month following that in which the return should have been filed until the last day of the month in which the return is actually filed; and

- A 10% surcharge from the first day of the seventh month following the expiry of the general six-month deadline; or

- A 40% surcharge if the declaration has not been filed within 90 days of receipt of a formal notice.

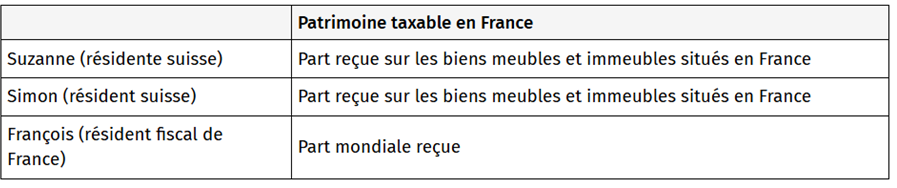

III – Summary case study (France-Switzerland)

Jacques, a French national, died on 11 September 2025 at his home in Montreux (canton of Vaud, Switzerland).

He is survived by:

- His wife Suzanne, a Swiss resident, to whom he was married under the regime of separation of assets; and

- Two children from a previous marriage, Simon, who lives in Switzerland, and François, who is completing his medical studies in Bordeaux.

During his lifetime, Jacques had drawn up a Swiss public will, in which he bequeathed one-third of his estate in full ownership to Suzanne and the remaining two-thirds to his two children. However, this will is silent about the Law applicable to his succession.

The estate consists of:

- A house in Montreux: €3 million;

- Financial assets in Switzerland: €10 million;

- A property in Bordeaux: €2 million; and

- Various movable assets in France: €150,000

Let us apply the suggested approaches step by step:

1ststep: putting together a qualified international team

Without delay, despite the pain of bereavement, Suzanne and her children will seek out professionals competent in cross-border estate settlement and international taxation, both in Switzerland and France.

2ndstep: determining the law applicable to the estate

From a French perspective, pursuant to the Rome IV Regulation, as the Habitual residence at the time of death was in Switzerland, Swiss law must apply. The fact that Switzerland is a non-EU country does not prevent this (Article 20 of the Rome IV Regulation, ‘Universal Application’).

From the Swiss perspective, under Swiss federal law, ‘the succession of a person who had their last domicile in Switzerland is governed by Swiss law’ (Federal Act on Private International Law, Art. 90).

Consequently, Jacques’s succession will unquestionably be governed by Swiss law.

3rdstep: checks regarding the reserved portion

Here, Jacques has clearly opted for an equal distribution of the estate. This is compatible with Articles 913 and 1094-1 of the French Code civil. There is therefore no conflict with mandatory French law. The estate will not be subject to the compensatory levy.

However, a number of assets are located in France.

4thstep: identifying the ‘UFOs‘

Switzerland, and more specifically the canton of Vaud, is a civil law jurisdiction whose inheritance rules are quite similar to those we are familiar with in France. Although certain specific legal structures or arrangements exist in Switzerland (such as trusts or foundations), Jacques had simply made provisions for his estate by signing a public will that is entirely comparable to our authentic wills.

The recognition and validity of this will with regard to assets located in France will therefore pose no problem. We can simply anticipate that the French notary will most likely ask his Swiss colleague to produce a certificate de coutume, or equivalent document, and that he will attach a copy of the public will to his own documents.

5thand6tsteps: verification of the scope of French tax and exclusion of a bilateral agreement

The specific Franco-Swiss bilateral treaty has unfortunately been revoked by France, meaning it no longer applies to these cross-border successions.

On the French side (i.e. with regard to the devolution of assets located there or the receipt of the inheritance by François), the taxable base must be clearly identified.

Switzerland will normally tax the entire estate (with the exception of immovable property situated abroad) and France, by default, movable and immovable property situated in France. The situation becomes somewhat more complicated for François, whose tax residence is in France. In his case, France may tax all the assets received in his capacity as an heir (he may, however, benefit from a tax credit limited to the tax paid in Switzerland in accordance with the common provisions of the CGI).

7thstep: filing an inheritance tax return and paying inheritance tax in France

Once the transfer of assets has been confirmed and the French Certificat de notoriété for this purpose, and in any event within one year of Jacques’s death, his heirs must file a complete declaration de succession. Suzanne will be exempt from tax as a widow, whilst Simon and François will have to pay tax according to the progressive scale for direct descendants (after personal allowances):

| Applicable rate | Applicable scale |

| Not exceeding €8,072 | 5% |

| Between €8,072 and €12,109 | 10% |

| Between €12,109 and €15,932 | 15 |

| Between €15,932 and €552,324 | 20% |

| Between €552,324 and €902,838 | 30% |

Conclusion

Cross-border inheritances are becoming increasingly common. However, the Civil aspects, as well as the Tax regime governing these inheritances, are still relatively poorly understood. Depending on whether they are handled professionally or not, they will be settled quickly whilst avoiding double taxation, or they will drag on and add to the distress of losing a loved one…

That is why we wanted to share these practical tips with our readers.

If you are involved in such an inheritance or wish to plan your own, we will be happy to answer any questions you may have.