1. Definitions

The trust is a well-known institution in Common Law countries (United Kingdom, USA, Australia, New Zealand, Caribbean countries and territories, etc.). It is also found in so-called “mixed” countries characterised by “bijuralism”, i.e. where the legal system is inspired by both Common Law and civil law (Mauritius, Seychelles, Saint Lucia, etc.). It is even found in some civil law countries, which officially recognise its effects and offer a framework adapted to its constitution, for various geographical and economic reasons (e.g. Monaco).

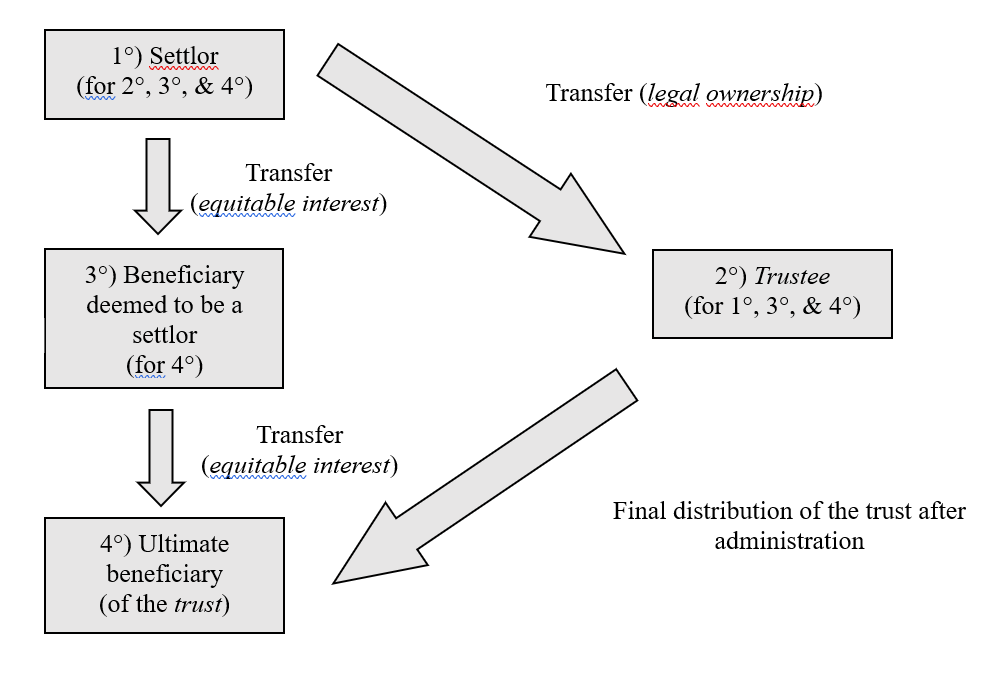

Trusts can be defined as the “legal relationships created – by inter vivos deed or on death – by a person, the settlor, when assets have been placed under the control of a trustee for the benefit of a beneficiary or for a specified purpose“1. It is therefore an arrangement whereby a person, known as the settlor, places certain assets in the interest of one (or more) other(s), known as the beneficiary(ies), under the control of a third party, known as the trustee, who is vested with certain powers of administration and/or disposal.

Trusts may be created privately (deed of trust, etc.), by court order or by operation of law. They may be created inter vivos (i.e. during the lifetime of the settlor, the beneficiary and the trustee) or mortis causa (i.e. when provided for in a will). Although trusts have always been used to manage assets and inheritance, their applications have become so diverse (financial, corporate, charitable, academic, etc.) that they have become a key institution in the “Anglosphere“.

2. French reluctance

Despite the widespread use of trusts, the French legal system is still quite reluctant to recognise them. Firstly, in 2007 France introduced the competing mechanism of the fiducie, which, although comparable, is not identical. This is because its scope is narrower (incompatible with gifts, succession…), its regulatory framework more restrictive and its effects different (no separation between legal and equitable ownership). Secondly, in 2011, France adopted a specific tax regime, which is characterised – it has to be said – by its harshness towards foreign trusts. In practice, the tax authorities and administrative courts adopt a generally defensive, even punitive, stance towards foreign trusts. Finally, France, although a signatory to the Hague Convention of 1 July 1985 on the law applicable to trusts and their recognition, has put off ratifying it ad vitam eternam.

This French mis-trust reached a climax when the great Magistrate Renaud Van Ruymbeke proclaimed that trusts should no longer exist in the 21st century2.

Trusts are thus perceived, without much nuance, as an instrument of concealment. It is increasingly becoming intolerable, at a time when ‘transparency‘ (which should apply primarily to the public sector…) is being erected as a totem, in defiance of the right – however fundamental3 – to privacy.

Given the large number of Anglo-Saxon expatriates living in France, it is certainly not unusual to come across trusts in France. The purpose of this series of articles is precisely to help expatriates understand how French law treats the trusts they have set up abroad.

3. Civil recognition of foreign trusts

Trusts do not exist in French law. Accordingly, it is not possible to set up, manage or dissolve a trust under French law.

However, there is nothing to prevent trusts set up abroad from being recognised and producing effects in France. Since the famous “Epoux Courtois et autres crts de Ganay” decision handed down on 10 January 1970 by the Paris Court of Appeal, French courts have given trusts a favourable reception, on two conditions:

- i) they have been validly constituted abroad; and

- ii) They do not conflict with French public policy.

By “favourable reception“, we mean the production of enforceable and effective legal effects in France, particularly in terms of transfer of ownership.

In civil law, the practice consists of:

- Comparing the concrete effects of the trust with well-known legal concepts in France, in particular gifts and inheritance; or

- “Welcoming‘ the trust as such”, i.e. by taking account of the specific features of the triangular relationship in light of the foreign law.

From a methodological point of view, a distinction must be made between the law applicable to the trust arrangement – that is to the instrument creating it (the instrumentum) – on the one hand, and the law applicable to the effects produced by the same trust regarding the transfer of ownership. This conflict of laws is significant in real estate matters (because of the rule lex rei sitae). This is why we generally do not recommend placing French real estate in a foreign trust. While it may seem perfectly normal, from an English or American point of view, to “place” all kinds of assetsin trust (including those situated abroad), the fact that trusts do not exist under French law should not be ignored.

To resolve this problem, our firm was able to advise the notary in charge of settling an international estate to treat the foreign trust as a classic operation of French law. A testamentary trust set up under New Mexico law was indeed treated as a universal legacy between spouses in order to allow the estate to be settled in favour of the widow.

Such a method of “assmiliation” is actually recommended by the Cour de cassation itself, in its famous “Wildenstein” decision4:

“…] according to the civil and tax case law of the Cour de cassation developed since 1996, it is appropriate to focus on the concrete effects of the trust concerned as established and governed by the applicable foreign law in order to determine whether it has effected, within the meaning of French law, for the benefit of the beneficiary or beneficiaries, a transfer of ownership which took effect on the death of the settlor and which is liable to be subject to duties on gratuitous transfers”.

Free translation

As each trust is different, the legal effects produced should be studied on a case-by-case basis (thanks to the international collaboration of lawyers) before deciding in favour of a particular method of “civil recognition” of the foreign trust.

4. Tax regime applicable to foreign trusts

4.1. Provisions resulting from the 2011 reform

Since the entry into force of the provisions of the amended Finance Act 2011-900 of 29 July 2011, foreign trusts have been subject to a specific tax regime, codified in Articles 750 ter, 752 and 792-0 bis of the General Tax Code and L. 19 of the Book of Tax Procedures.

This regime applies rationae temporis to gifts made and deaths occurring on or after 30 July 2011.

The tax rules applicable in France are autonomous and independent of the legal characteristics of the trust under the foreign law under which it was set up. It is therefore sufficient for the legal relationship to correspond to the definition set out in Article 792-0 bis of the General Tax Code for the new regime to apply, regardless of the name given, whether or not it is revocable, etc. :

“Trust” means all legal relationships created under the law of a State other than France by a person who has the status of settlor, by inter vivos deed or mortis causa, with a view to placing assets or rights therein, under the control of an administrator, in the interest of one or more beneficiaries or for the achievement of a specific objective.

Free translation

As the tax regime applicable to foreign trusts is complex, the following presentation is by no means exhaustive, as the format of this article allows only the broad outlines to be given. Certain overriding rules may apply depending on the country in which the trust was set up (countries considered non-cooperative).

4.2. Tax treatment of cash distributions

Beneficiaries often receive certain fruits, income and/or interest generated by the trust assets. These are known as periodic distributions, as opposed to the final distribution, dissolution, or winding-up of the trust.

As long as the beneficiary is an individual domiciled in France within the meaning of French tax regulations, he or she is taxed on these sums as income from capitaux mobiliers (Art. 120, 9° of the General Tax Code). This is a general rule, so the origin of the income distributed has no impact on its classification as income from capitaux mobiliers.

Such income is now subject to the flat-rate withholding tax of 30%.

It is important to note that trust income is very rarely covered by international tax treaties. For example, the French tax authorities consider that such income is excluded from the Franco-British treaty of 19 June 20085. The risk of double taxation must therefore be seriously considered, if possible right from the constitution stage.

4.3. Tax treatment of gifts or inheritances made through trusts

When the trust assets are allocated to the beneficiaries, the tax treatment of this transfer will depend on whether it is treated as a gift or an inheritance.

According to case law, this is the case when:

- The assets leave the trust and are allocated to the beneficiaries6; or

- The assets remain in the trust and are not terminated on the death of the settlor, unless the settlor has actually divested himself of the assets7.

In practice, most of the foreign trusts we come across in France are comparable to gifts or inheritances. It is therefore this tax regime that we will present here.

When such is the case, the transfer of the assets or rights placed in the trust and the income capitalised therein is subject to the general system of duties on gratuitous transfers for their net market value at the date of transfer. These duties vary depending on the relationship between the settlor and the beneficiary8.

Rates applicable in direct line9:

| Fraction of net taxable share | Applicable rate in % |

| Not exceeding €8,072 | 5 |

| Between €8,073 and €12,109 | 10 |

| Between €12,110 and €15,932 | 15 |

| Between €15,933 and €552,324 | 20 |

| Between €552,325 and €902,838 | 30 |

| Between €902,839 and €1,805,677 | 40 |

| More than €1,805,677 | 45 |

Rates applicable between collateral relatives and between non-relatives10:

| Fraction of net taxable share | Applicable rate in % |

| Between living or represented brothers and sisters: | |

| Not exceeding €24,430 | 35 |

| More than €24,430 | 45 |

| Between relatives up to and including the 4e degree | 55 |

| Between relatives beyond the 4e degree and between non-relatives | 60 |

Where the settlor and the beneficiary are married, the transfer of assets to the beneficiary following the death of the settlor is exempt from transfer duties under article 796-0 bis of the French General Tax Code11. Partners who have entered into a civil partnership abroad also benefit from this exemption, provided that their partnership is not contrary to French public policy12.

In order for these transfer duties to be levied, the criteria for the territoriality of transfer duties (set out in Article 750 ter of the French General Tax Code) must be met (since, as we have seen, bilateral agreements do not generally cover trusts).

4.4. Specific rules for dynastic trusts

Some trusts may continue for several generations (known as “dynastic trusts“). When such is the case, the beneficiary may, on the death of the settlor, be considered as a new “settlor for tax purposes“. This system makes it possible to apply transfer duties to each successive transfer. Here, it does not matter whether the transfers meet the conditions for classification as gifts and/or inheritance: where the trust continues over several generations, the first beneficiary or beneficiaries are deemed to be settlors and transfer duties are payable again on their death.

4.5. Reporting obligations of trustees

Where the settlor or at least one of the beneficiaries is resident in France for tax purposes (as at 1er January), trustees are subject to two reporting obligations13

They are first subject to a declaration relating to the creation, modification or termination of the trust (known as an “event declaration“). Information on the terms of the trust and the identity of the beneficial owners must be provided.

Secondly, an annual declaration of the market value as at 1er January of the assets and rights placed in the trust and their capitalised income, to be filed by 15 June of the year14 (known as the “annual declaration of value“).

These two declarations must be completed in French on a form n°2181-TRUST1 (event declaration) or n°2181-TRUST2 (annual declaration) and filed with the foreign company tax department15.

Failure to comply with these reporting obligations may result in severe penalties, such as a fixed fine of €20,00016, certain solidarity mechanisms between settlors and beneficiaries deemed to be settlors, or an 80% surcharge calculated on the duties due in the event of adjustments to real estate that should have been reported.

4.6. Trusts and the French wealth tax

Under article 970 of the French General Tax Code, real estate assets that fall within the scope of the real estate wealth tax (“IFI”) and that are placed in a trust are included in the assets of the settlor, or in those of the beneficiaries deemed to be settlors, at their net market value on 1er January of the tax year.

For the purposes of the IFI, the trust becomes transparent, so to speak: the settlor is subject to the IFI as if the trust did not exist. If there are several beneficiaries deemed to be settlors, the real estate assets are deemed to be divided equally between them, unless otherwise stipulated in the deed of trust.

Conclusions

As our readers will no doubt have realised, foreign trusts are rather unfavourably welcomed in France. From the many civil headaches involved (how to recognise and enforce their effects?) to the complex tax regime resulting from the 2011 reform, French tax residents are generally advised not to set one up.

The fact remains that many expatriates are settlors, beneficiaries or even trustees of an arrangement established in accordance with their national law. Trusts being complex tools, they warrant professional legal advice. Citizen Avocats can help you to :

- Ensure compliance with your tax and reporting obligations;

- To facilitate the production of positive legal effects, notwithstanding the absence of French equivalence; and

- Minimise the risk of conflict between the various players in the trust.

- Art. 2 of the Hague Convention of 1 July 1985 on the Law Applicable to Trusts and on their Recognition ↩︎

- in Offshore : Dans les coulisses édifiantes des paradis fiscaux, Editions Les Liens qui Libèrent, 2022 ↩︎

- “Everyone has the right to respect for his private and family life, his home and his correspondence“, Art. 8 European Convention on Human Rights ↩︎

- Cass. Crim. 6 January 2021, n°18-84.570 ↩︎

- BOI-INT-CVB-GBR-10-20 n°470 ↩︎

- Cass. com. 15th May 2007 n°05-18.268; Cass. com. 18th November 2020 n°18-11-2020; Cass. com. 6th November 2019 n°17-26.985 ↩︎

- Cass. Crim. 6 January 2021, no. 18-84.570 ↩︎

- Art. 792-0 bis II of the General Tax Code ↩︎

- Art. 777 of the General Tax Code ↩︎

- Art. 777 of the General Tax Code ↩︎

- BOI-ENR-DMTG-30 n° 90 ↩︎

- BOI-ENR-DMTG-10-50-30 n°40 ↩︎

- Art. 1649 AB of the General Tax Code ↩︎

- Art. 369 A, ann. II of the General Tax Code ↩︎

- Art. 369 and 369 A ann. II of the General Tax Code ↩︎

- Art. 1736 IV bis of the General Tax Code ↩︎