If you do business in France, you have probably heard of “holding companies“. There are many reasons why this is a popular topic: whether it is to optimise the management of a group of companies or to facilitate reinvestment, it has many advantages.

This management and investment tool is indeed essential for any investor with a long-term vision.

On the one hand, it offers several advantages in terms of managing, protecting, and passing on assets to heirs, whatever the type of investment (II). On the other hand, it is a powerful fiscal and financial lever: systematic in the case of business investments, yet relative in the case of property investments (III).

But first, a few definitions are in order (I).

I. What is the point of a holding company?

Holding companies are corporate vehicles whose main purpose is to hold equity interests in other legal entities. Therefore, the term “holding company” does not refer to a specific form of company per se, but to the way in which it is used.

Holding companies usually take the form of a Société civile (comparable to UK partnerships), Société à Responsabilité Limitée (standard companies with limited liability) or Société par Actions Simplifiée (joint stock companies very close to the English Private Ltd companies).

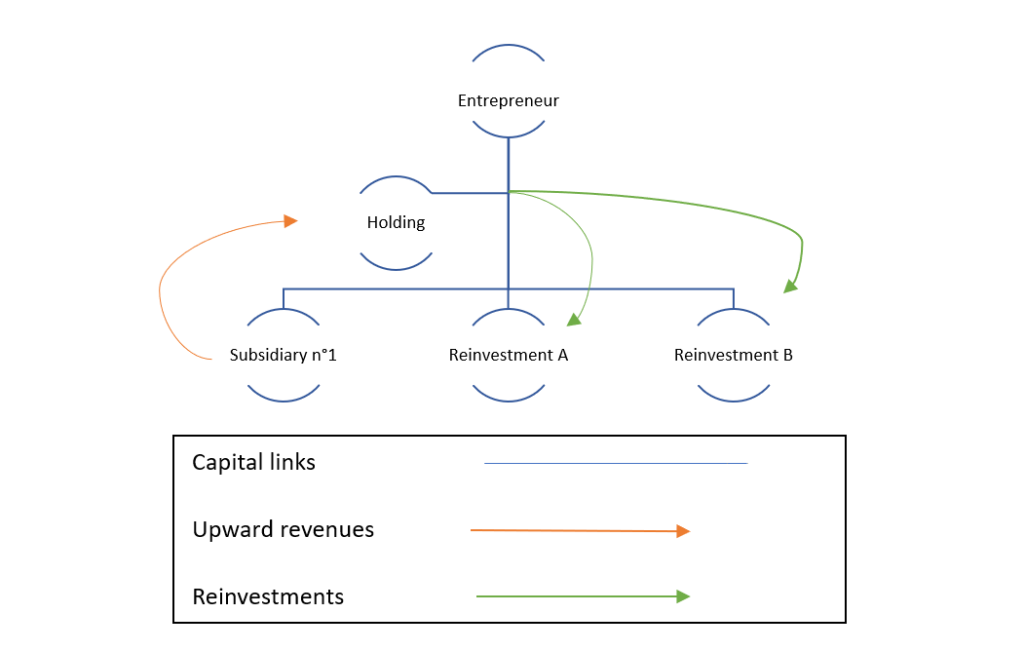

It can be set up before or after investing:

- Prior to any investment: the entrepreneur brings equity to the holding, or make it borrow money from banks, allowing it to invest in several subsidiaries or assets, corresponding to various investments;

- After having already made investments: the entrepreneur transfers the shares he/she held within the existing companies to the holding, in exchange for shares in the latter. In this case, the holding will continue to support ongoing investments and will invest in new projects.

This type of structuring has two main characteristics. Firstly, by being placed above a group of companies each corresponding to different investments, the holding company centralises all the holdings within a single entity. Secondly, it recovers the benefits of its investments in the form of:

- Dividends;

- Services billed to subsidiaries (e.g. legal, accounting, management, etc.); and/or

- Executive remuneration (when designated as legal representative of its “daughter companies”) within each subsidiary.

As we shall see, this flow of money to the holding company (and not to the investor directly) greatly facilitates new investments.

II. Holding companies are an effective tool for managing, protecting, and passing on assets to heirs

As we shall see, the holding company has many advantages in terms of estate planning, when major investments have been made during the entrepreneur’s lifetime.

Whatever the type of investment, this vehicle makes it easier for the heirs to manage it (2.1.), as well as protects the estate (2.2.).

It also helps to optimise taxation, regarding gifts and inheritance tax (2.3.).

2.1. Facilitating the management of assets by the heirs

Unlike a holding company, which can be passed down through generations, entrepreneurs are not immortal. The question of estate planning is inevitable. So, it is best to be well prepared.

If an entrepreneur has decided to invest without holding company, two major problems may arise for the heirs: joint ownership (i.e. in French “Indivision”) and dispersal.

Serge BRAUDO’s legal dictionary defines joint ownership as follows:

“Joint ownership is the situation in which there are assets over which rights of the same kind belonging to several people are exercised (…) Joint ownership usually results from the law, as in the case of heirs before they have divided up the assets of the estate“.

In short, this is the concurrent right of ownership exercised by several people in respect of the same assets. This is the case for heirs following a death, in respect of the deceased’s property (real estate, company shares, etc.). This situation lasts until:

(i) the heirs divide up the assets of the estate, or

(ii) even sometimes after the heirs have divided up part of the estate, where it is provided that they shall remain in joint ownership.

The problem arises when the heirs do not get along well with each other, because in principle, 2/3 of the joint owners are required to take joint decisions (for the most trivial matters), and sometimes unanimously (for the most important, such as selling the property concerned) [1].

Holding the assets through a holding company tends to avoid this pitfall, since only the company’s capital (and not the investments held by the holding company) will be subject to joint ownership. In that case, the articles of association and/or a shareholders’ agreement will provide a safe framework related to investment management, eventually until the heirs manage to divide up the shares: for example, by appointing a director in charge of managing the assets according to certain rules laid down by the deceased.

It is even possible to avoid joint ownership, notably by transferring all or part of the holding company’s capital to one or more specific heirs before death! [2] In this case, the heirs are not competing for the same shares, but each holds a certain number in full ownership. Instead of requiring a 2/3 majority or unanimity, decisions will be taken solely in application of the articles of association and shareholders’ agreement, whether at the level of the management in place, or at the level of shareholders’ decisions: clauses governing partners’ decisions, appointment of a “wise” manager of the holding company (who may, to a certain extent, be irremovable) to guarantee the continuity of investments, etc.

In addition, the risk of dispersal is encountered when there are multiple companies and in the absence of appropriate succession planning. The heirs, who have become partners, are then dispersed among multiple companies, each with a very distinct activity. The situation is particularly problematic in the event of disagreement or even dispute between the heirs, as the overall operation of the group becomes incoherent and inefficient.

Here again, the holding company avoids this problem, since all the heirs are partners “at the top“, within the holding company, allowing a more centralised and coherent management policy for the group as a whole.

2.2. Protecting the entrepreneur’s personal assets

Investing as an individual implies bearing the associated risks personally. Accordingly, in the event of excessive indebtedness, or even cessation of payments, creditors can seize the entrepreneur’s entire assets (company shares, real estate, etc.).

A holding company in the form of a SARL or SAS protects personal parties’ assets. This is because only the holding company will be liable for its losses, as the liability of its shareholders is limited to their contributions. Where the subsidiaries also have limited liability, each of them will be liable for its own debts, again with no effect on the assets of the holding company or the entrepreneur.

However, this is not the case for holding companies set up in the form of civil companies, since their partners are subject to unlimited personal liability. This is why SAS or SARL companies are generally more suitable for setting up a holding company.

2.3. Optimising gift and inheritance tax for heirs

If one is not careful, in the case of investments in the real economy (i.e. commercial, industrial, agricultural, liberal or craft activities, etc.), direct transfer by way of gifts or inheritance can, in practice, means the end of the business. As direct gifts or inheritance tax can be as high as 45% of the value of investments in the family line, heirs sometimes have no choice but to sell or dismantle the business to pay it off.

To alleviate this problem, the legislator introduced the so-called “DUTREIL Pact“. In simple terms, heirs benefit from a 75% allowance when calculating gift/inheritance tax, subject to the company shares being held for a certain length of time[3] .

In most cases, this system applies to holding companies[4], insofar as they own other entities with predominant operational activities.

Besides, whether the investments are made in the real economy or in real estate, the holding company allows other types of optimisations regarding gift/inheritance tax:

- Heirs can acquire an interest in the capital as soon as the holding company is set up[5], and will thus be allocated shares in full ownership, representing a fraction of the group (in which case there will be no transfer by gift or death);

- The donor can give his children shares in the holding company, worth a total of 100,000 euros per beneficiary every fifteen years, with total exemption from gift tax, enabling the group to be passed on gradually to the heirs;

- This progressive donation can be further enhanced by:

- A dismemberment of the ownership of the shares between usufruct (to be retained by the donor) and bare ownership (to be passed on to the beneficiary). The bare ownership passed on having less value than full ownership, it is possible to give more shares every fifteen years, and to benefit from the combination of usufruct and bare ownership at the time of death, with exemption from inheritance tax[6],

- A discount of 10% to 15% of the value of the shares passed on to the heirs, because the assets are held by the company and not by the entrepreneur personally[7], which means that more shares can be given away every fifteen years.

III. Unavoidable fiscal and financial leverage

Holding companies provide systematic tax and financial leverage when investing in companies (3.1.), however, this leverage must be put into perspective when investing in real estate (3.2.).

3.1. Business investment: the advantages are unquestionable

The equation is mathematical:

- As an individual shareholder (situation of the entrepreneur, in the absence of a holding company), receiving dividends from a company subject to corporation tax (IS) gives in principle rise to payment of the 30% “flat tax”[8] ,

- As a corporate shareholder subject to corporation tax (the holding company), receiving dividends from this same company gives rise to a total tax of 1.25%.

This is thanks to the “mère-fille” regime, whereby, under certain conditions, only 5% of the dividends received by the holding company will be subject to the French corporate income tax (i.e. 15% on the first €42,500 of profits and 25% thereafter) and the remaining 95% will be exempt.

This tax relief within the holding company means more equity to reinvest!

The same applies torevenues earned by the holding company in the form of management fees or services invoiced to subsidiaries: their maximum corporate tax will be 25%, whereas the maximum income tax for individuals is 45%.

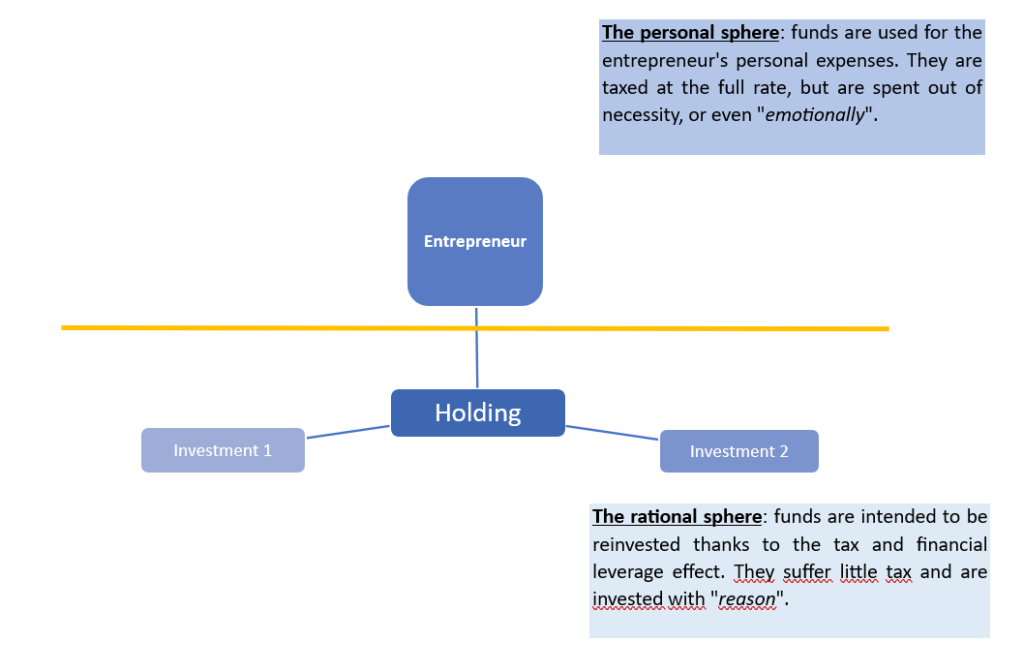

Of course, this leverage effect is only of interest if the entrepreneur plans to reinvest. If he/she withdraws the gains from the holding company by way of personal dividends, these will be taxed at 30%.

Conversely, if he/she reinvests this capital in subsidiaries placed under the holding company,[9] he/she should not have to pay any more tax than the 1.25% above. The goal here is to facilitate the reinvestment of the holding’s trésorerie in a cost-effective manner. By contrast, what is paid into the hands of the entrepreneur is not intended to be invested, but rather spent (living expenses, leisure activities, etc.). Indeed, let’s not forget that before the entrepreneur actually receives this income, he/she will have to pay tax on it at a rate of 30% (dividends), or even up to 45% (income as an individual director or salaries subject to the progressive tax scale). Similarly, if he/she keeps these funds in savings until his/her death, his/her heirs will pay inheritance tax of up to 45%… Even more reason to take advantage of this non-invested income during one’s lifetime!

Another important point: capital gains tax on the sale of shares held by a holding is 3%, compared to the 30% tax applicable where the seller is an entrepreneur without a holding… That being said, holding is not a choice, but a must-do!

3.2. Real estate investment: the benefits are not systematic

Every entrepreneur is, at some point, concerned about retirement. This is one of the reasons why many of them turn to real estate investments. They may be attracted by a certain stability, ease of management, as well as anticipation of risks that are generally well known, compared with financial investments…

In France, such investments are often made via a société civile immobilière (SCI). SCIs are intermediary companies between the holding company or the entrepreneur and the property, designed to hold and manage real estate.

3.2.1. Rental income

In terms of tax on rental income, the usefulness of the holding company is relative. Let’s compare the tax consequences of having a holding depending on the situation of the entrepreneur:

- Tax on rental income is exactly the same whether the investment is made directly by a holding company subject to corporation tax, or by a SCI held by a holding company subject to corporation tax:

In any case, profits will be subject to corporate income tax, at the level of the holding company[10], with no tax on dividends as long as the capital does not leave the holding company[11].

On the other hand, if the rental concerns furnished accommodation, the SCI held by a holding company will itself be subject to corporation tax at the rates mentioned above. Dividends paid to the holding company will then be subject to the 1.25% “mère-fille” rate referred to in section 3.1.

Dividend payments from the holding company to the investor are always subject to the “flat tax” of 30%.

- The tax treatment of rental income from a civil company owned directly by the entrepreneur is as follows:

If the property is let furnished: the SCI is subject to corporation tax (i.e. 15% – 25%) and the dividends paid to the entrepreneur are subject to the flat tax (30%);

If the rental is unfurnished: in principle, the SCI is not subject to corporation tax and the income is taxed directly in the hands of the entrepreneur at the personal income tax rate (0% to 45%), plus social security contributions at 17.2%.

- Taxation of rental income when the entrepreneur holds the property directly without a company is as follows:

If the rental is furnished:

The entrepreneur can choose to be taxed on an actual basis and accordingly deduct depreciation and management costs, as well as loan interests, each year before rents are subject to the income tax rate (0% to 45%),

Conversely, he/she can opt for a “micro-BIC” tax regime (if the rental income is less than €77,700), and benefit from a flat-rate allowance of 50% on the rental income before it is subject to the income tax rate (0% to 45%),…

… he/she obviously won’t have to pay tax on dividends, in the absence of an interposed company between him/her and the leased property…

… but will be subject to social security contributions nonetheless in addition to the personal income tax: in the case of LMP[12] , approximately 45% and in the case of LMNP, 17.2%

If the rental is unfurnished: income is subject to the income tax rate (0% to 45%), plus social security contributions at 17.2%.

3.2.2. Capital gain on resale

The usefulness of holding company should also be put into perspective regarding taxation of capital gains on property sale. Let’s compare the following situations:

- For the main place of residence, buying in one’s own name is more efficient

Personal owners benefit from a total exemption from capital gains tax on resale[13]. A contrario, this very important exemption does not apply if the property is held via a company subject to corporation tax[14]. Please note that this does not prevent you from purchasing your main residence via an SCI, as long as it’s not subject to corporation tax[15] and not placed “under” a holding subject to it. Such an acquisition via an SCI can indeed be useful in order to benefit from the advantages described in point 2 above.

It should be added that owning your main residence in one’s own name, or through an SCI subject to personal income tax does not require you to pay rent. On the contrary, if the property is held by a holding company subject to corporation tax, the investor must pay rent to this company in order to avoid any abus de droit fiscal or unlawful use of corporate assets[16] .

Of course, to buy such residence, the entrepreneur would appreciate being able to benefit from the leverage effect described in 3.1. They might be tempted to distribute dividends from their operating company to their holding company in order to reinvest these funds in their principal residence under the holding company (thus avoiding the “flat tax”). Nevertheless, the calculation in regard to the cost of this reinvestment and the tax payable on capital gains on resale often comes out in favour of direct investment. In other words, an immediate gain may not be so profitable in the long term.

- For rented properties, it all depends on the type of tenancy

In the case of furnished rentals:

When the property is directly or indirectly held by a holding company subject to corporation tax, or held without a holding company but via an SCI subject to corporation tax: the holding company or the SCI is taxed on the difference between the sale price and the net accounting value of the asset (less depreciation), at a rate of 25%.

When the property is held directly, i.e. without a company, in the case of LMNP, the entrepreneur will be taxed on the difference between the sale price and the acquisition price (without deducting depreciation), at the rate of 19% tax and 17.2% social security contributions, with the possibility of total exemption from tax and social security contributions if the property is held for more than 30 years.

If the property is held directly, in the case of LMP, the entrepreneur will be taxed on the difference between the sale price and the net accounting value (after deducting depreciation), at a rate of 12.8% for income tax and 17.2% for social security contributions[17], with a possible total exemption if the rental income is less than €90,000 per year over the previous 2 calendar years and if the rental activity has been carried out for more than 5 years[18] .

For unfurnished rentals :

Where the asset is held by a holding company subject to corporation tax (i.e. when held by the holding company itself or by an SCI not subject to corporation tax placed under the holding): the holding company is taxed on the difference between the sale price and the net accounting value of the asset (less depreciation), subject to corporation tax (15-25%).

When the investor buys directly without a holding company, or via an SCI not subject to corporation tax, the entrepreneur will be taxed on the difference between the sale price and the purchase price (without deducting depreciation), at a rate of 19% personal income tax and 17.2% social security contributions, with a possible total exemption from tax and social security contributions if the property is held for more than 30 years.

What can we conclude from all the above? While the holding company is an essential tool for professional investments, it is not always true for real estate investments. In this second hypothesis, only a detailed study, considering the type of property, its use and the investor’s plans (annuity for retirement, planned resale in the long term, etc.), can determine whether a holding company subject to corporation tax is appropriate.

Théo J. LE FLOHIC

Citizen Avocats

[1] In the case of a non-trading property company (SCI) under a holding company: a non-trading property company (SCI) that is not subject to corporation tax (IS) is semi-transparent for tax purposes; its partners (in this case the holding company) are therefore taxed on their share of profits, according to their own tax regimes (in this case corporation tax). In real estate, the SCI will not be subject to corporation tax if the rental activity does not involve furnished accommodation; otherwise, the SCI itself will be subject to corporation tax.

[2] Otherwise taxed at 30% at contractor level.

[3] The LMNP (Loueur en Meublé Non Professionnel) scheme applies to the letting of furnished accommodation by an individual, where the income generated by the letting does not exceed €23,000 per year for the owner and 50% of the owner’s total income per year. The LMP (Loueur en Meublé Professionnel) scheme also applies to furnished lettings, but above the two aforementioned thresholds.

[5] Which is normally the case with a holding company

[6] Articles 150U and 150UB of the CGI

[7] As the funds come from a holding company subject to corporation tax, which is usually a commercial company, the absence of rent paid to the entity that owns the property risks being classified as a tax abuse, or even a misuse of corporate assets.

[8] “Long-term” scheme, if the property is held for more than two years. In this case, social security contributions do not apply. The system is different for short-term capital gains (held for less than two years).

[9] Article 151 septies of the CGI.

[10] 12.8% tax and 17.2% social security contributions

[11] In the form of a capital contribution, a partner’s current account, etc.

[12] Article 815-3 of the French Civil Code.

[13] In particular, by means of gifts that benefit from certain transfer tax exemptions, or by giving certain heirs a stake in the holding company right from the incorporation stage.

[15] In all cases for group holding companies. As for passive holding companies, it is applicable within the limit of two levels of interposition with companies having a preponderant operational activity.

[16] Shares cost less to create, as the holding company’s net assets are not yet very high.

[17] There is none when usufruct and bare ownership are combined.

[18] Discount allowed by the tax authorities.